OP

OP

Zeno

Ancient

No, I haven't. I'll have to look into it. Any tips or pointers to info?

edit: and if the IRS is giving backdoors and info on them then they should just change the rules. More bureaucratic nonsense from our government.

Rather than me trying to explain it here are some good links that explain it much better than I ever could.

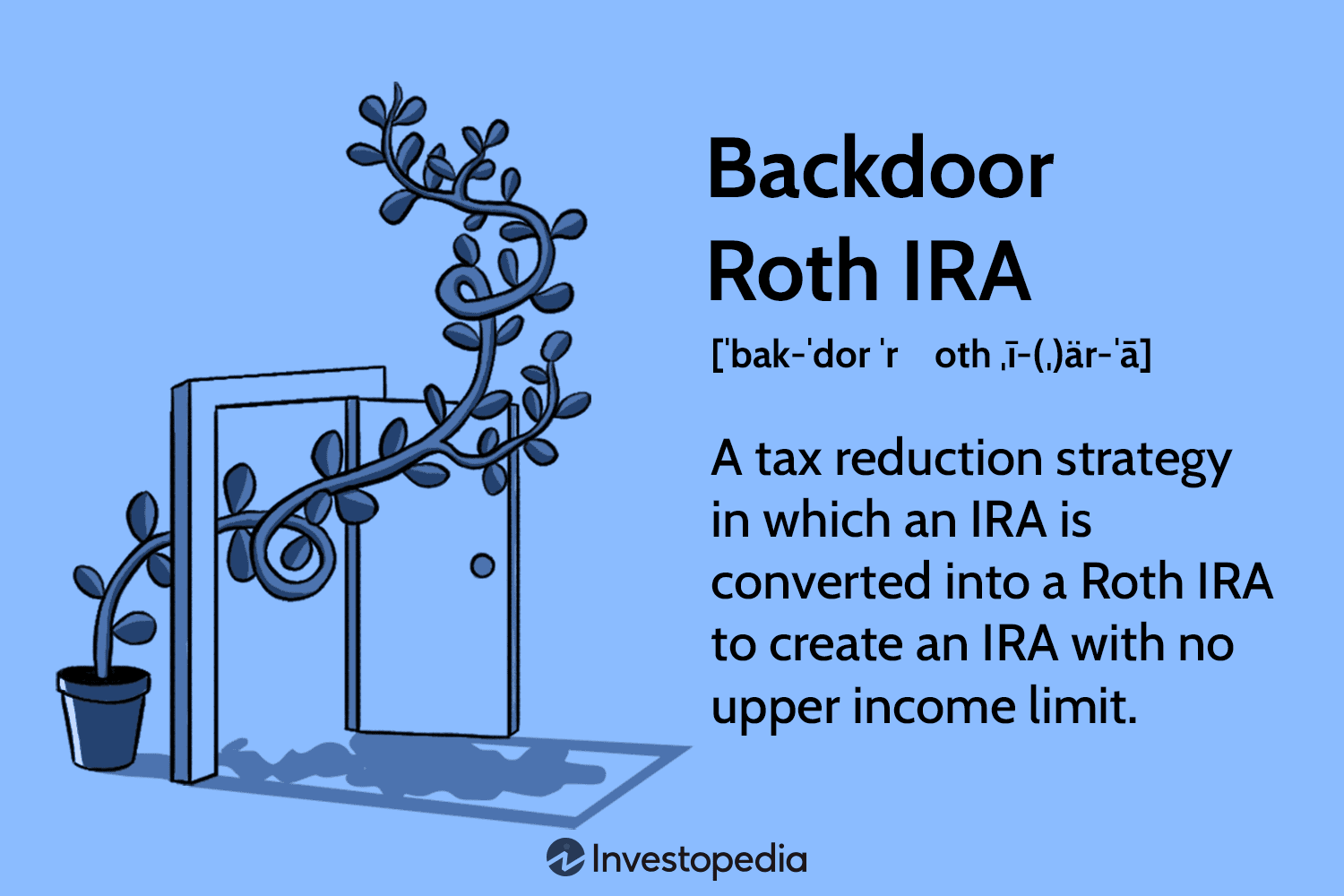

Backdoor Roth IRA: Advantages and Tax Implications Explained

Learn the updated 2025 backdoor Roth IRA strategy step‑by‑step—from contribution limits and MAGI thresholds to tax filing and avoiding pro‑rata rule traps.

Backdoor Roth IRA: What It Is, How to Set It Up - NerdWallet

A backdoor Roth IRA is a way to convert a traditional IRA into a Roth IRA. This may be an option if you make more than the Roth IRA income limit, but there are rules.

Basically your broker will open a traditional IRA you deposit your after tax money in there and immediately transfer it to the Roth (or any time before it earns any interest--if it earns any interest before you transfer you will have to pay tax).